A lot of business owners open an insurance audit notice and immediately assume something has gone wrong.

Usually, it hasn't.

An insurance premium audit is often a routine part of commercial coverage. If your policy started with estimated payroll, sales, square footage, hours worked, or similar exposure figures, the insurer may review what occurred during the policy term and adjust the final premium accordingly. For a busy SME, that can feel disruptive. But the process is far more manageable when you treat it as a records-and-controls exercise instead of a surprise investigation.

That shift in mindset matters. The companies that struggle most aren't always the ones with the biggest exposure changes. They're often the ones that can't quickly explain payroll, subcontractor use, job duties, or accounting records.

The Audit Letter Arrived Now What

The envelope lands on your desk. Your first thought might be, "Why are they auditing us?"

A better question is, "What records will help us close this out cleanly?"

For many SMEs, the notice arrives after a hectic stretch of hiring, seasonal work, contract labor, or changing revenue patterns. A firm that added field staff, used subcontractors for overflow work, or split employees across office and operational roles may not have every detail neatly organized. That's why the letter feels heavier than it is.

Why the notice feels more serious than it is

A premium audit isn't the same as an accusation of wrongdoing. In plain terms, it's a reconciliation. The insurer started with estimates. Now it wants the actual figures that match the policy period.

That means the process usually turns on documentation, not drama.

Keep this perspective in mind: the audit asks, "What was your real exposure during the policy term?" It does not automatically mean, "What did you do wrong?"

A common example looks like this. A business estimated payroll conservatively at the start of the year. Midyear, it added more staff and used a few uninsured subcontractors during a rush period. Nothing improper happened operationally. But the final premium may change because the business activity changed.

Your first moves should be practical

When the letter arrives, resist the urge to guess your way through it. Pull together the policy, note the audit period, and assign one person to coordinate records. If your files are spread across payroll, bookkeeping, HR, and operations, start gathering them immediately.

If part of your challenge is locating past records from different systems or custodians, a records support workflow such as specialized record retrieval services can help organize the paper trail before the audit turns into a last-minute scramble.

A calm response usually beats a fast one. Read the notice carefully, confirm deadlines, and start building one clean audit file.

Understanding the Insurance Premium Audit

An insurance premium audit is the settlement step that converts an estimate into a final number.

When a carrier issues certain commercial policies, it often doesn't yet know your exact annual payroll, sales, or other exposure base. So it prices the policy using projected figures. After the policy term ends, the audit compares those estimates with actual business activity and recalculates the premium from the audited exposure using the contract rate, as explained in the CAS actuarial discussion of audit premiums and New York Regulation 129.

Think of it like an estimated utility bill

If you've ever received a utility bill based on estimated usage and then later seen an actual meter read, the logic is similar. The earlier charge kept service moving. The later review settles the account.

In insurance, that "meter read" is your real exposure during the policy period.

The result can go in any direction:

- Additional premium due if actual exposure was higher than estimated

- Refund or credit if exposure was lower

- No change if the estimate was close to reality

What exposure means in practice

Exposure depends on the line of insurance and the nature of your business. Workers' compensation often ties to payroll. General liability may use sales, square footage, or other operational measures. The point isn't just volume. It's what kind of work happened, how labor was classified, and whether records support those distinctions.

For businesses in regulated industries, transportation, field services, or operations with variable staffing, it also helps to understand the broader insurance requirements tied to your activities. A practical reference is My Safety Manager's insurance guide, especially if your company has operational exposures beyond a standard office environment.

Practical rule: If the premium started with an estimate, assume the insurer may later ask you to prove the actual numbers behind that estimate.

Why this is more than an internal carrier preference

In some markets, the audit isn't merely customary. It has formal timing and compliance significance. The same actuarial source notes that New York's Regulation 129 requires the audit within 180 days after policy expiration for eligible commercial policies written on an estimated exposure base, unless a narrow exception applies.

That matters because many owners still think the audit is optional or informal. Often, it isn't.

If your finance and operations data live in different places, a structured back-office process such as insurance services BPO support can make the eventual reconciliation much cleaner. The core issue isn't just record storage. It's whether payroll, class descriptions, and accounting data line up in a way an auditor can follow.

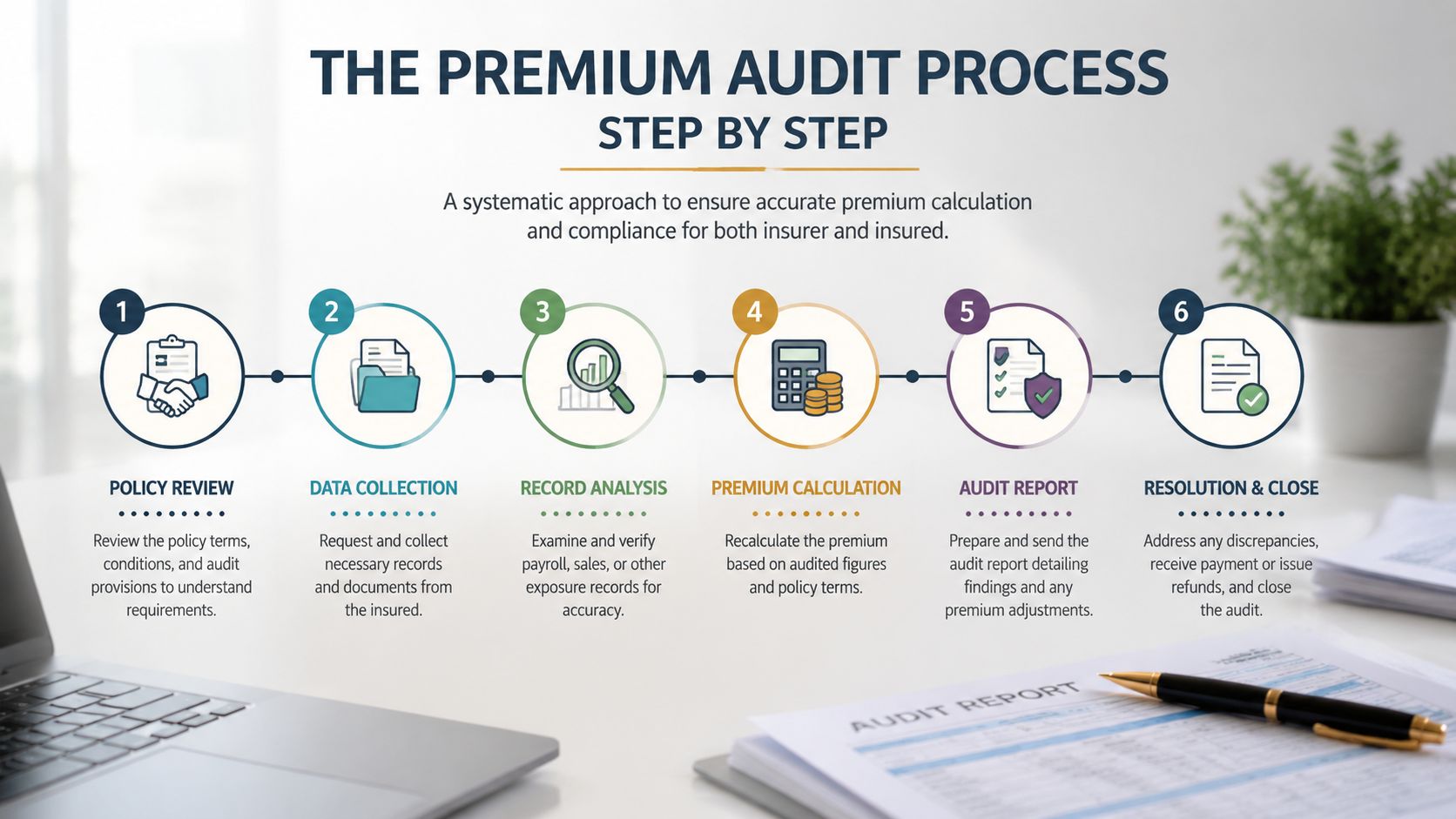

The Premium Audit Process Step by Step

Most premium audits follow a recognizable sequence. Once you know that sequence, the process becomes easier to manage.

According to Hotchkiss Insurance's overview of premium audits, the exposure base is usually tied to the line of business. Workers' compensation is most commonly based on payroll, while commercial general liability may use sales or square footage. The audit process typically collects records such as payroll reports and tax filings, and after review the insurer may increase, decrease, or leave the premium unchanged.

Step 1 Notice and audit type

The process begins with a notice after the policy expires. That notice usually identifies the policy period under review and tells you how the audit will be handled.

Common formats include:

- Mail or self-report audit for simpler accounts

- Virtual audit using uploaded documents and remote review

- Physical audit when operations are more complex or records need closer examination

The format changes the workload, but not the central question. The auditor still needs enough documentation to verify actual exposure.

Step 2 Record collection

Next comes the document request. At this juncture, many SMEs either stay in control or fall behind.

The auditor may ask for payroll records, tax documents, sales support, ledgers, subcontractor information, or role descriptions. If your bookkeeping and payroll teams maintain separate naming conventions, this is often where mismatches show up. An employee coded one way in payroll but described differently in operations can create avoidable confusion.

Step 3 Classification review

This step tends to cause the most misunderstanding.

The auditor doesn't just total your numbers. The review also looks at how payroll or other exposure should be assigned. If one employee performed both clerical and field work, or if staff shifted into different job duties during the year, classification becomes important. The same issue can apply to subcontractors and uninsured labor.

The final premium isn't only about how much activity occurred. It's also about how that activity was classified and documented.

Step 4 Recalculation of premium

Once the auditor verifies the exposure base, the carrier recalculates the premium under the policy's rating structure. This is the settlement point.

You may receive:

- An additional bill if your actual exposure exceeded estimates

- A credit or refund if the estimates were too high

- A no-change result if records align closely with the original basis

Step 5 Review the statement carefully

When the audit statement arrives, don't just look at the amount due or credited. Read the assumptions behind it.

Check whether:

- Payroll matches your records

- Sales or other exposure figures cover the correct period

- Subcontractors were treated correctly

- Employee roles reflect what people did

Step 6 Close the loop internally

A premium audit shouldn't end with payment or dispute resolution alone. It should also trigger internal cleanup.

If the auditor struggled to trace payroll or contractor support, that tells you something useful about your systems. Businesses that fix those issues after the first difficult audit usually handle the next one with far less friction.

How to Prepare Your Audit Documentation

Preparation starts long before the auditor asks for anything. The strongest audit files are built during the year, not reconstructed after the fact.

A practical insurance premium audit file should let an outside reviewer trace numbers from summary reports back to source records. If payroll totals don't reconcile to tax filings, or subcontractor payments can't be matched to certificates of insurance, the review becomes harder and the risk of unfavorable assumptions rises.

What auditors are usually trying to verify

The records themselves matter. So does the logic connecting them.

Auditors commonly request payroll reports, overtime earnings, quarterly tax filings, general ledgers, profit-and-loss statements, and certificates of insurance for subcontractors to verify that exposure data is complete, traceable, and properly classified, as described in Stolly's explanation of premium audit preparation. That same source notes that some carriers cite a 60 to 90 day window for completion, which is why contemporaneous records matter so much.

If you have to rebuild payroll history from memory, spreadsheets, and email threads, you're already on weak footing.

Essential Audit Documentation Checklist

| Document | What It Proves | Preparation Tip |

|---|---|---|

| Payroll reports | Total wages paid during the policy period | Match employee names, dates, and departments to your internal roster |

| Overtime records | Whether overtime was tracked separately | Keep overtime identifiable rather than merged into regular pay |

| Quarterly tax filings | Payroll totals reported to tax authorities | Reconcile filing totals to payroll summaries before audit season |

| General ledger | How compensation and contractor costs were booked | Use consistent account names across the year |

| Profit-and-loss statements | Revenue and expense context for the business | Make sure the statement period matches the policy term |

| Subcontractor certificates of insurance | Whether subcontracted labor should be excluded from your exposure base | Collect and file certificates before work begins, not after payment |

| Job descriptions and role summaries | Why employees belong in one class rather than another | Update descriptions when duties change, not only at hiring |

The records that usually create trouble

Three categories deserve extra attention.

- Subcontractor files. If a subcontractor performed work and you can't produce a current certificate of insurance, the auditor may treat that labor differently than you expected.

- Mixed-duty employees. A vague title like "operations support" doesn't tell the auditor whether someone was clerical, technical, field-based, or supervisory.

- Expense support. Cash disbursements and supporting receipts often help explain contractor spend and operational costs. If your team needs a refresher on organizing expense proof, ReceiptGen's guide to expenses is a useful primer on what clean documentation should look like.

Build one audit file, not five partial ones

A strong audit packet usually includes a single folder structure by policy year, with payroll, tax filings, general ledger support, subcontractor COIs, and role descriptions all in one place. That sounds simple, but many businesses still keep those records across email, payroll portals, shared drives, and paper folders.

The easier you make the auditor's path, the easier it is to support your own position.

Common Audit Pitfalls and Costly Mistakes

The most expensive audit problems usually aren't exotic. They're ordinary recordkeeping failures that change how labor or revenue is interpreted.

In workers' compensation and general liability policies, the audit recalculates premium using verified payroll, sales, and class codes. Shifts in job duties, overtime, subcontractor spend, or misclassified employees can materially change premium. For SMEs, the most audit-sensitive inputs are payroll segregation, job descriptions, and subcontractor certificates of insurance, as outlined in AmTrust's audit process explanation.

What happens if a subcontractor has no COI

This is one of the most common pain points.

You hire a subcontractor for overflow work. The invoice gets paid. The work is done. Months later, during the audit, no one can find a certificate of insurance proving that subcontractor carried its own coverage.

The issue isn't just administrative. Without the COI, the auditor may include that labor in the exposure base reviewed under your policy. That can affect the final premium.

Prevention is simple, but it requires discipline:

- Collect before work starts rather than chasing paperwork later

- Check that the certificate matches the work period

- Store certificates with vendor records, not only in email

What happens if employees wear multiple hats

SMEs often run lean. One employee might do customer support in the morning, warehouse work in the afternoon, and onsite visits when needed. Operationally, that flexibility makes sense.

From an audit standpoint, it creates ambiguity.

If payroll isn't clearly segregated and role descriptions are weak, the auditor may not have enough basis to assign labor the way you intended. Broad, unclear coding can push payroll into a less favorable class treatment.

Good payroll coding isn't clerical housekeeping. It's evidence.

What happens if overtime and remuneration aren't organized

A messy payroll file can create unnecessary premium friction even when total wages are accurate. If overtime, bonuses, and other pay elements are buried in lump-sum payroll summaries, the auditor has less ability to review them properly.

That doesn't mean every pay category changes premium the same way. It does mean poor visibility makes your file harder to defend. The cleaner the segregation, the better your position.

The mistakes that repeat most often

Some patterns show up again and again:

- Using vague job titles that don't explain actual duties

- Booking subcontractor costs inconsistently across accounts

- Waiting until year-end to gather missing support

- Letting HR, payroll, and accounting use different labels for the same role

These aren't large strategic failures. They're process gaps. Fixing them usually requires tighter coordination between operations and finance, not more paperwork for its own sake.

Turn Audit Stress into Strength with an Outsourcing Partner

A difficult audit often reflects a deeper issue. The business doesn't have a clean, ongoing system for payroll coding, document retention, subcontractor compliance, and accounting reconciliation.

That's why audit prep feels painful. The company is trying to build controls after the fact.

Why daily process matters more than last-minute cleanup

When payroll, bookkeeping, and vendor records are maintained in separate silos, the audit exposes every disconnect. The owner asks accounting for payroll support. Accounting asks HR for classifications. HR asks operations what people did. Operations points to a spreadsheet that doesn't match the ledger.

An outsourcing partner can solve that at the process level by creating one governed workflow for recordkeeping, reconciliation, and support.

This matters even more as audit workflows become more digital. According to Happiest Minds' review of emerging technology in premium audits, technologies such as AI, RPA, and cloud tools can reduce manual audit effort by up to 80% and cut intake time by 80 to 90%. Faster intake helps, but it also means poor classifications and missing records can move through the process faster unless the data is governed well from the start.

What a good outsourcing setup actually improves

The benefit isn't just labor savings. It's operational consistency.

A well-run outsourced finance function can help with:

- Payroll coding discipline so labor categories stay consistent across periods

- Subcontractor compliance tracking so COIs are collected and retained systematically

- Ledger alignment so payroll, contractor costs, and financial statements reconcile cleanly

- Document readiness so audit support isn't buried across inboxes and local files

For teams that want stronger structure in day-to-day accounting operations, outsourced finance and accounting services are worth considering because they address the root cause of audit friction. The audit itself is only the symptom.

Why a USA-based outsourcing partner can be especially useful

For SMEs, using an outsourcing partner from the USA can make a practical difference. Communication is usually easier during business hours. Documentation expectations are often more aligned with U.S. insurance, payroll, and accounting workflows. And when an audit request needs a quick response, access and accountability tend to be clearer.

That doesn't make the audit disappear. It makes the business better prepared for one.

A strong partner helps you move from scattered files to controlled records, from role ambiguity to documented classifications, and from end-of-year panic to routine readiness. That's the value.

Conclusion From Reactive Fear to Proactive Control

An insurance premium audit can feel disruptive when it arrives as an isolated event.

It feels very different when you see it as the final checkpoint on data your business should already understand.

The smoothest audits usually come from ordinary habits: accurate payroll coding, clear job descriptions, organized subcontractor files, reconciled ledgers, and timely record retention. None of that is glamorous. All of it matters. When those controls are in place, the audit becomes less of a negotiation and more of a confirmation.

That's the practical lesson for SMEs. You don't need to treat the insurance premium audit as a threat. You need to treat it as a business process that rewards clarity.

If your records are messy today, that isn't a verdict. It's a starting point. Tighten the file structure. Make payroll classifications more precise. Collect COIs before work begins. Reconcile support before year-end instead of after the audit notice appears. Those steps improve both financial control and audit outcomes.

The businesses that handle audits best usually aren't lucky. They're prepared.

If your team wants help building cleaner payroll records, stronger subcontractor documentation, and audit-ready finance operations, NineArchs LLC can help with scalable back-office support. For a consultation, call (310)800-1398 / (949) 861-1804 or email [email protected].